The Market Minute - March 2023

Key Points

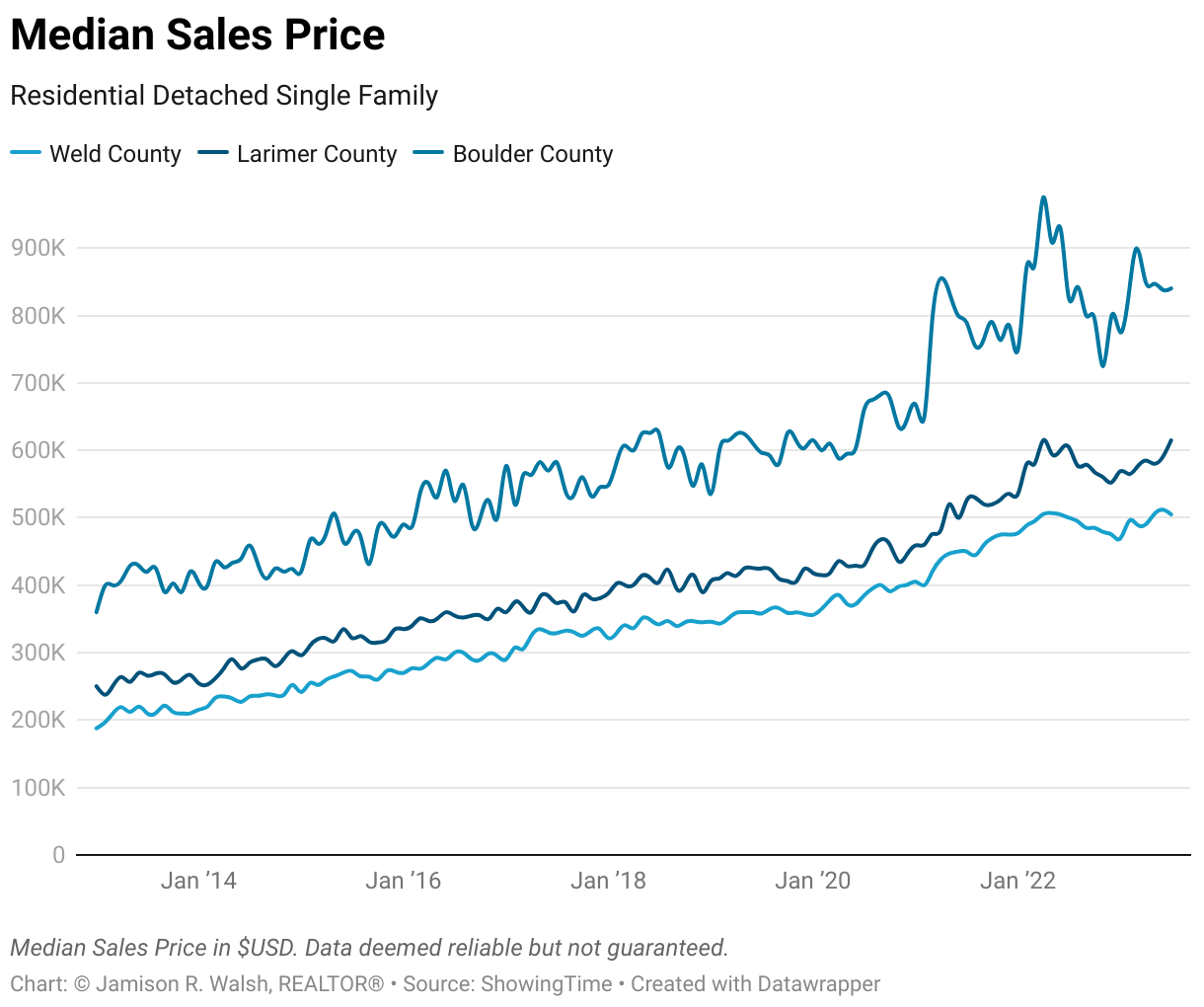

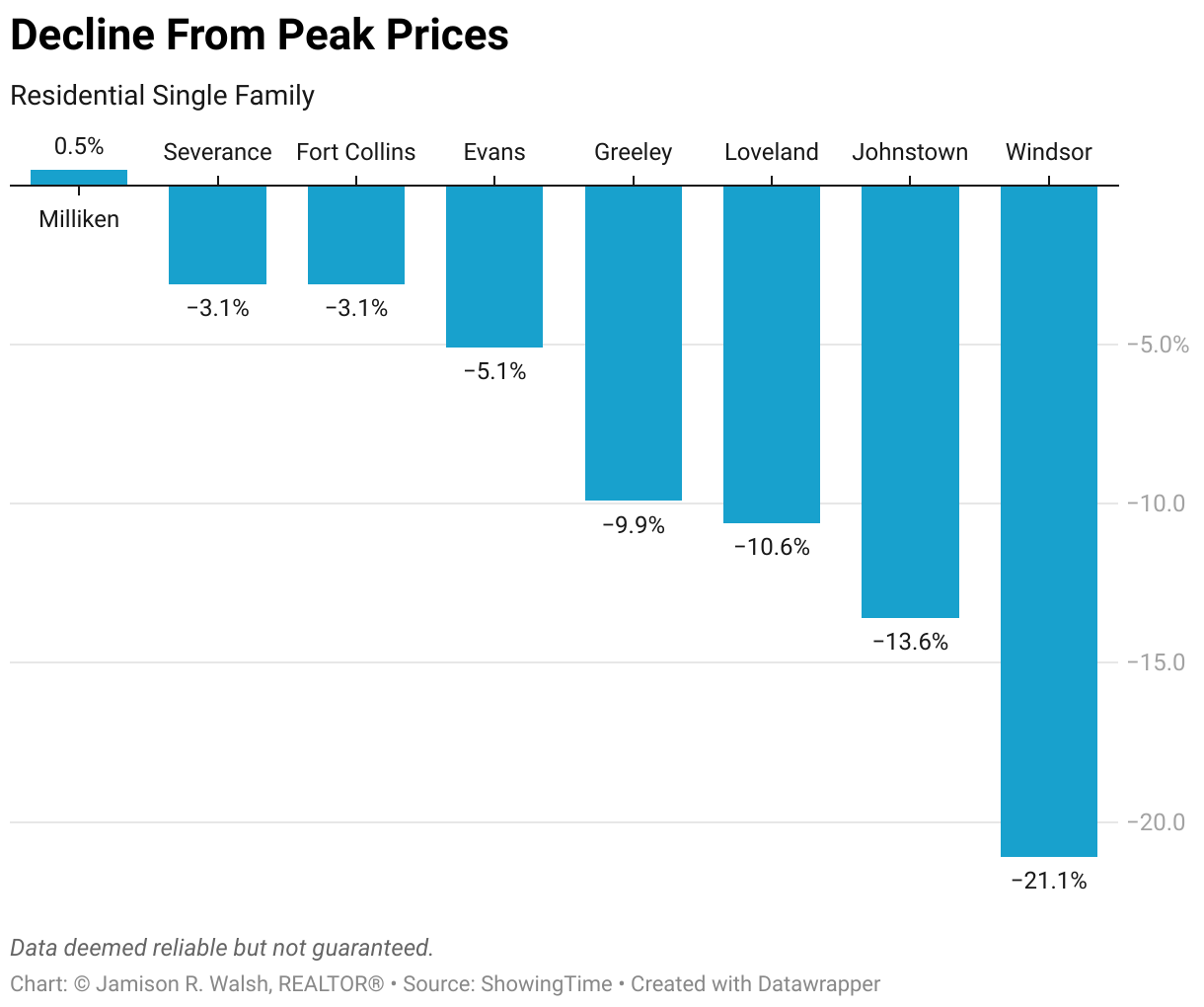

Median Sales prices in Northern Colorado stabilized in March, but with the exception Milliken, every metro across the region is still trending below peak prices from Spring 2022.

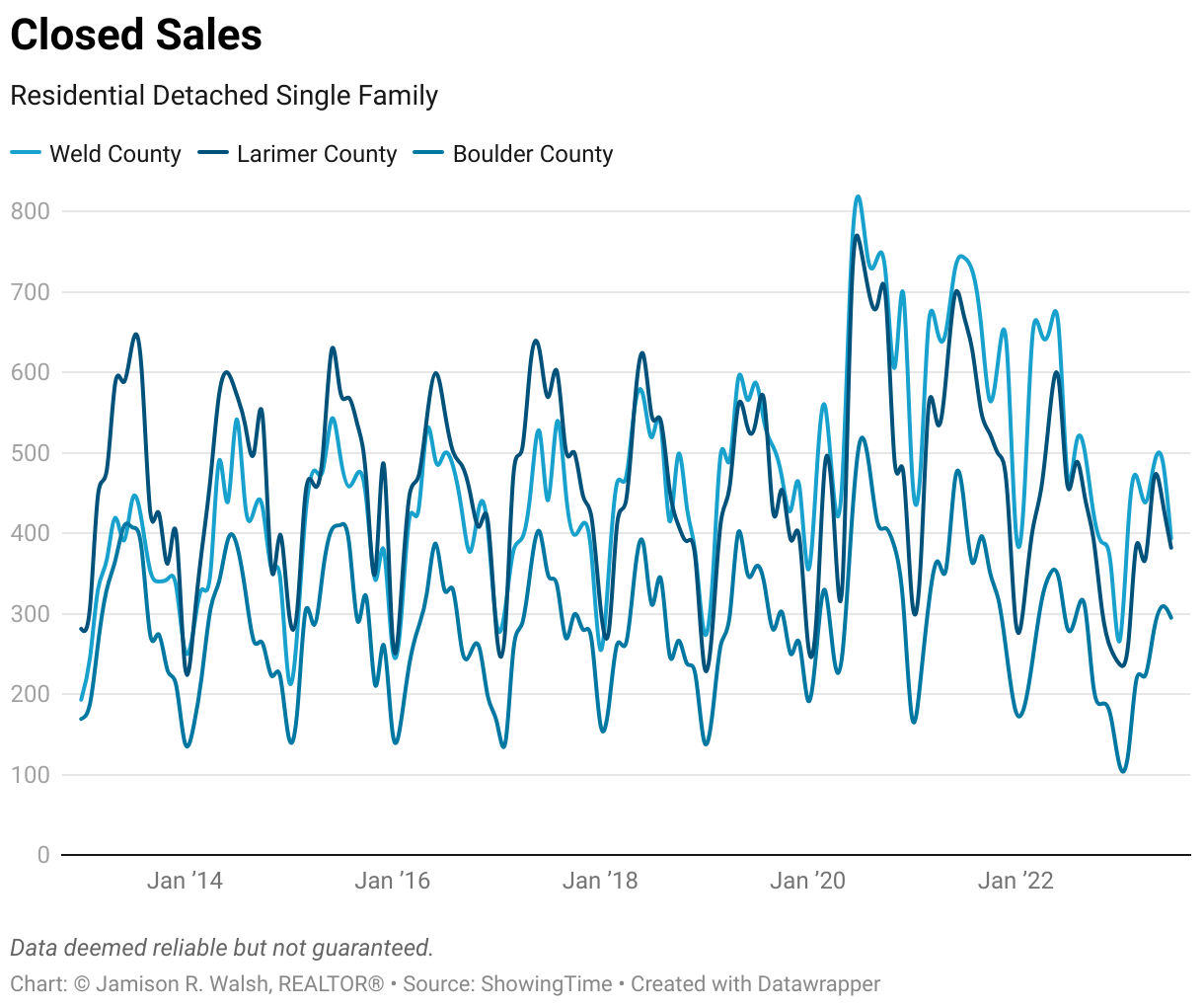

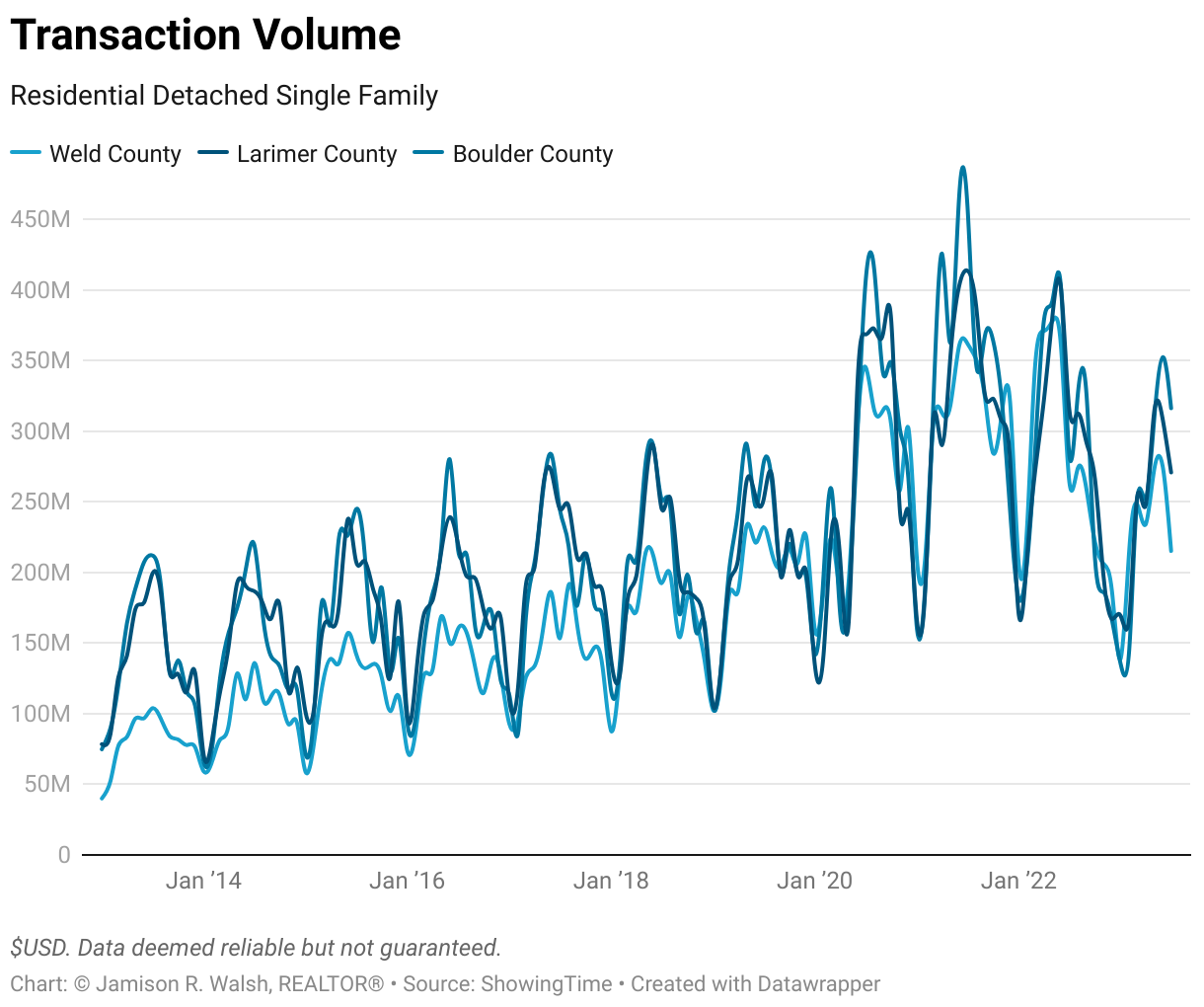

Housing market activity remains stagnant, with transaction volume barely above the levels of March 2020, a period in time where nearly the whole of the country was being forcibly quarantined.

A bifurcated housing market has emerged, with regions where home values are the most detached from the underlying fundamentals seeing the biggest retraction in home values since the peak in Spring 2022.

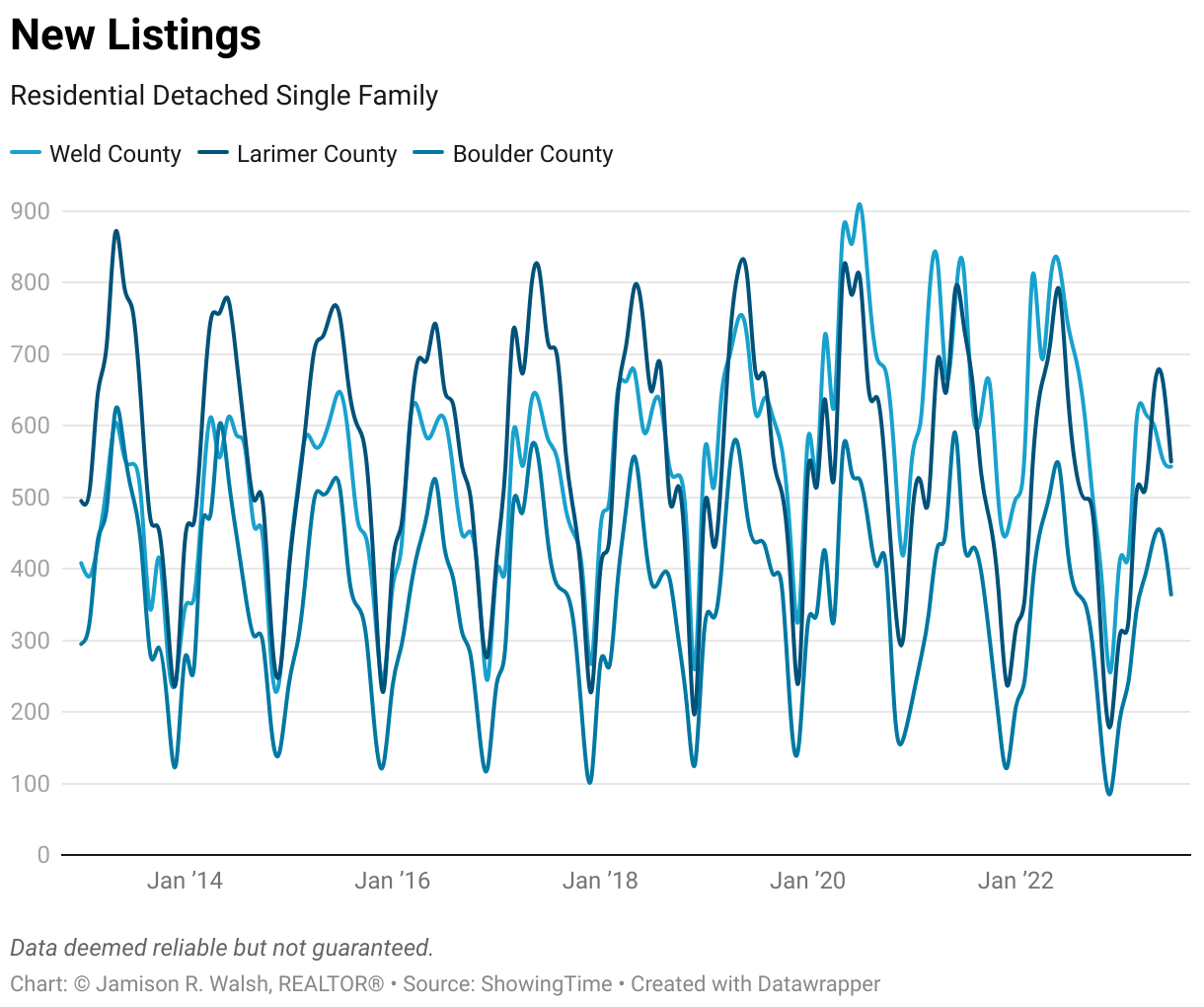

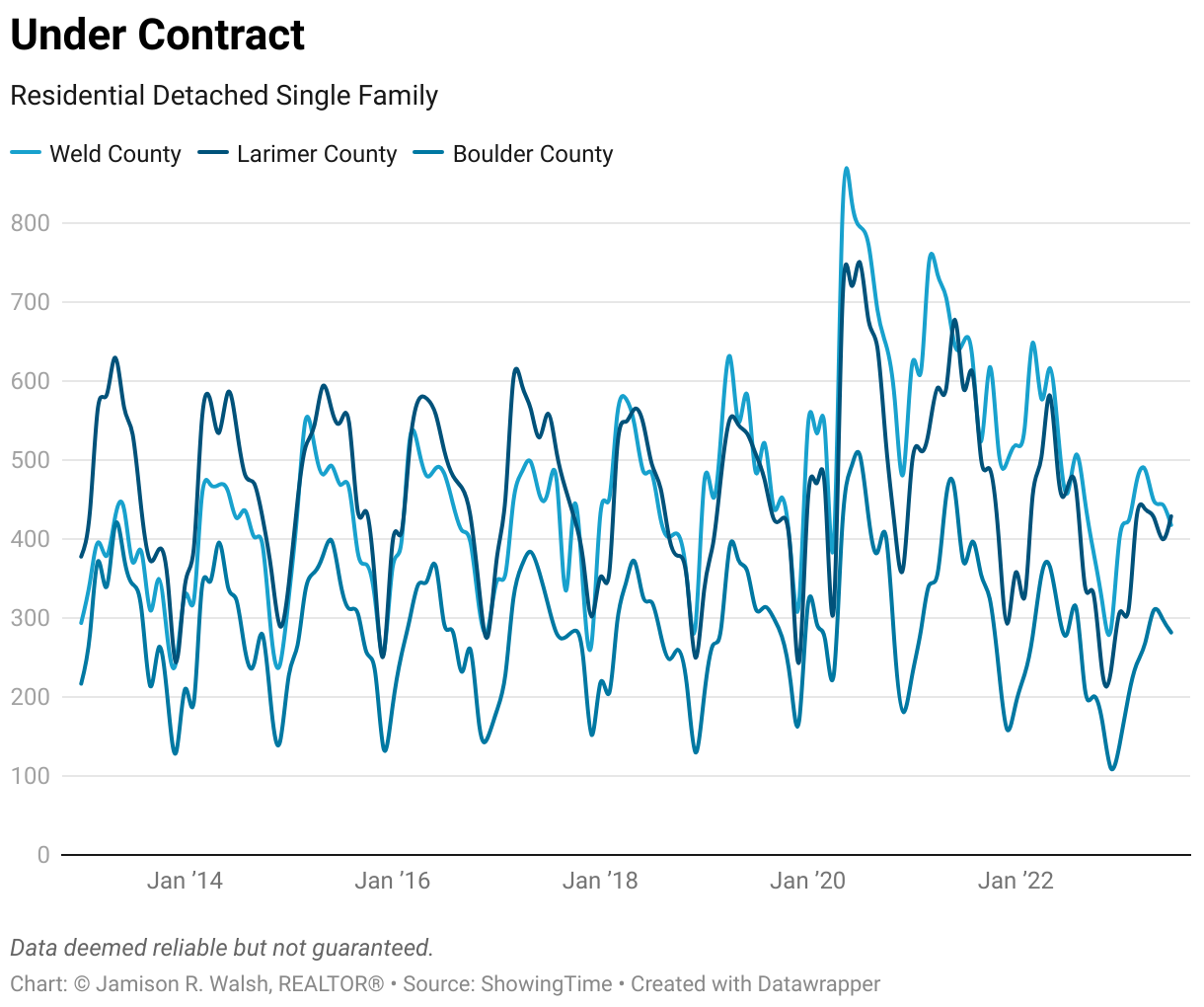

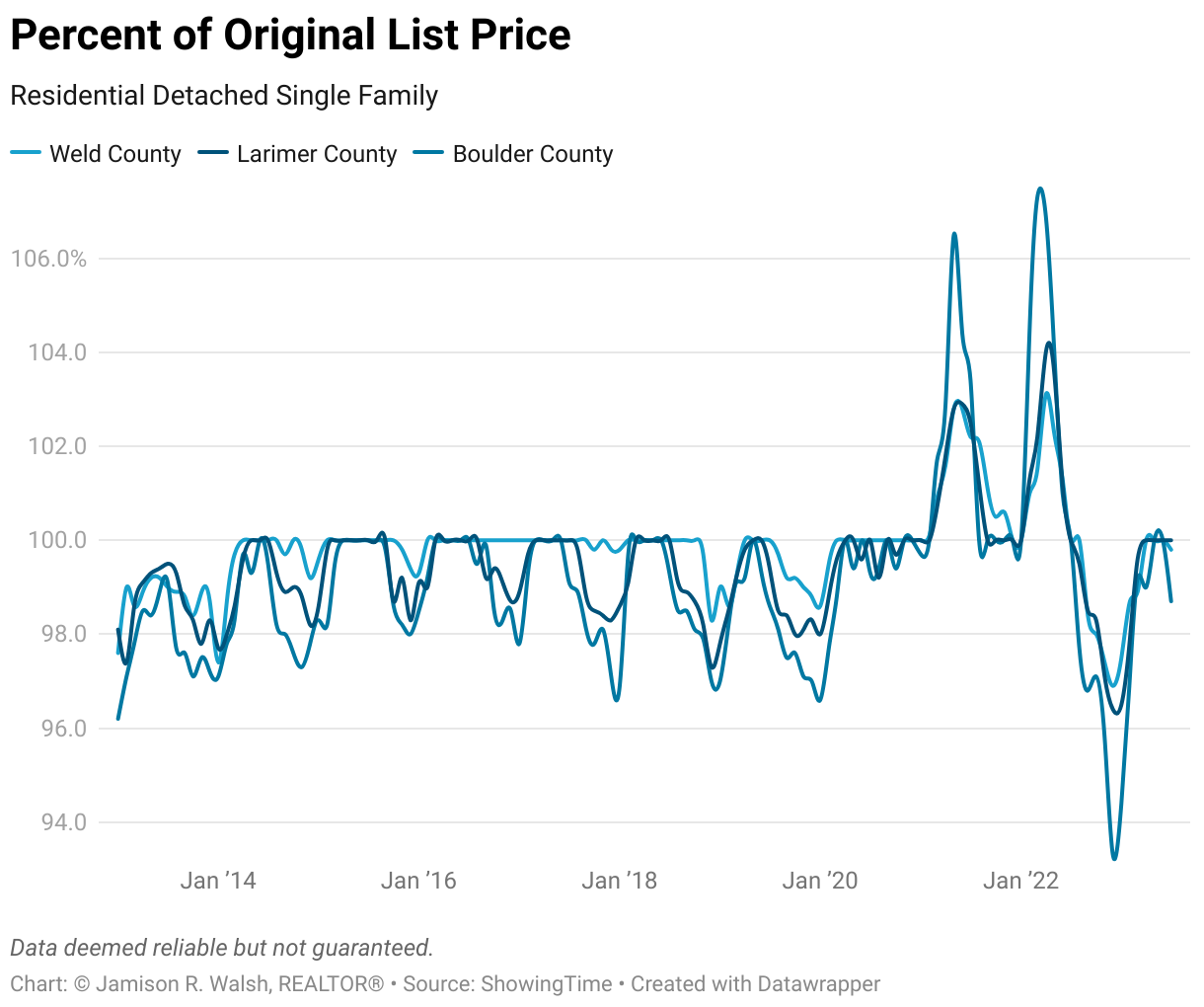

March continued to provide ambiguous signals for the Northern Colorado housing market. On one hand, the slip in Median Sales Prices, which recovered slightly in February, continued to gain ground in Larimer and Boulder Counties in March, but on the other hand, prices retracted again in Weld County. Likewise, across the region we saw a healthy uptick in new listings, available inventory, homes contracted for sale, and homes sold. However, these metrics still lag far behind their historical averages for the region. All this, combined with continued volatility in interest rates continued to keep buyers sidelined as they continued to wait out the market. This resulted in a continuation in the decline in the already battered market activity for the region, as reflected in the total transaction volume, with volumes for the entire region still lagging both year-over-year (YoY) and longer term historical averages.

Nationally, existing home sales jumped 14.5% month-over-month (MoM) in March, the first monthly gain in 12 months, representing the largest monthly increase since July 2020, according to the National Association of REALTORS® (NAR). The sudden uptick in sales activity stems from contracts signed toward the beginning of the year, when mortgage rates dipped to the low 6% range, causing a surge in homebuyer activity. Pending sales have continued to improve heading into spring, increasing for the third consecutive month, according to NAR.

The Bifurcated Market

At the national level, there are two distinct housing market beginning to emerge. These markets could generally be divided into the East and the West, with many Eastern markets enjoying a boom in both home sales and continued home price appreciation, and many Western markets experiencing very much the opposite. This bifurcation is highly problematic for those seeking to diagnose the overall health of the housing market at the national level. However, a cursory exploration of the data explains the reasons for this phenomena quite easily: the markets that saw home prices skyrocket the most since 2020 are now seeing the most significant declines.

A new report by data analytics provider CoreLogic reveals in many ways a tale of two very different housing markets. At one extreme, the West is slowing, and at the other extreme, the East is rising.

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

– Selma Hepp, Chief Economist for CoreLogic

For those of you that have been paying attention, you already know that I’ve been arguing that this eventuality was almost guaranteed given the meteoric rise in home values in the Northern Colorado region over the past 3 years. Local economic fundamentals, including income levels, have been completely detached from home values since the start of Pandemic Housing Boom in 2020. The shift in monetary policy that began in 2022 and drove borrowing costs through the roof, combined with dwindling personal savings, increasing economic uncertainty and 40-year high inflation are all now colliding with these fundamentally detached home values. Case in point, as we round the corner to the one-year anniversary of peak home values for most regions (which occurred from April to July 2022 for most metros), the negative YoY appreciation is finally starting to catch up to the negative drop form peak prices:

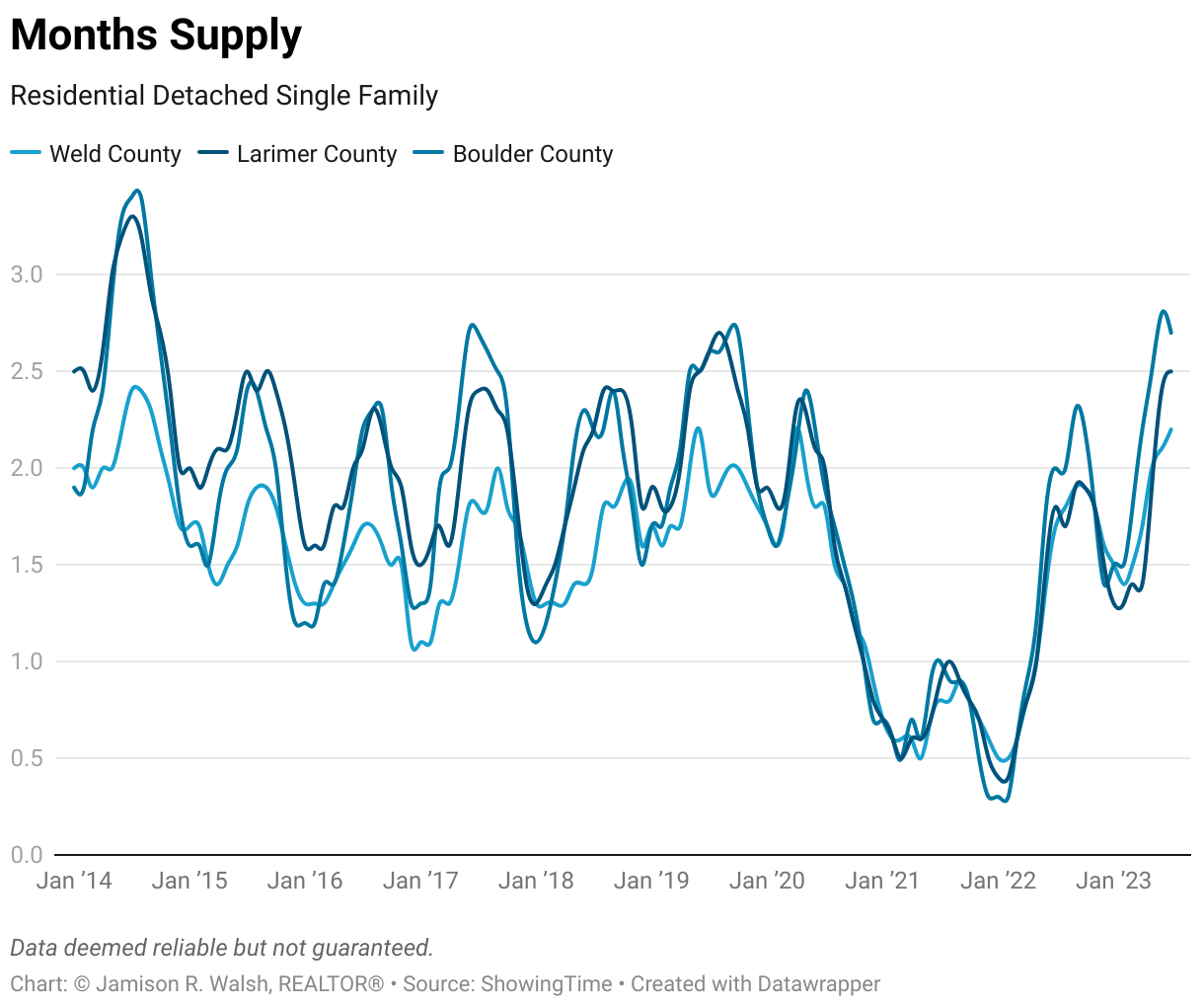

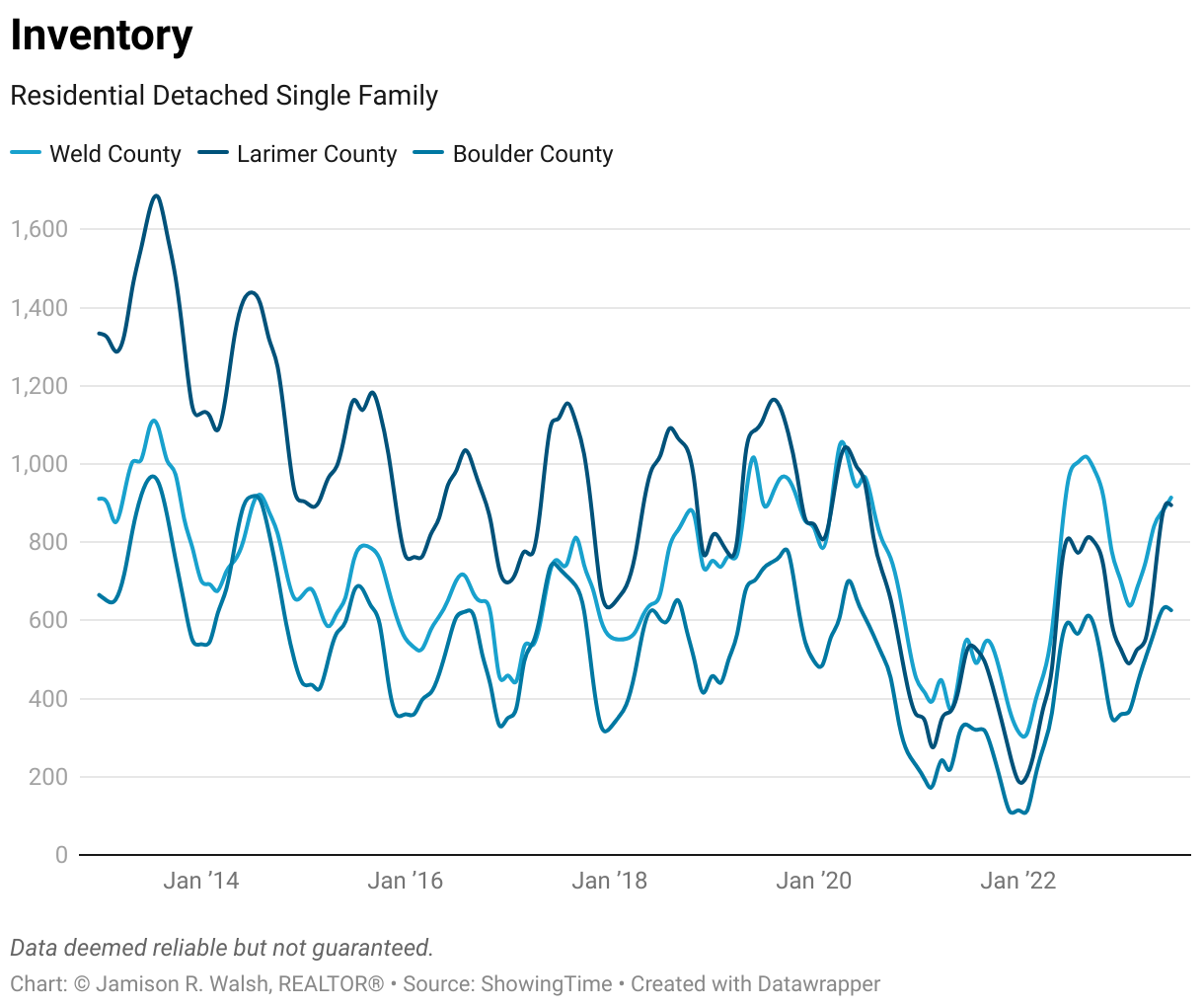

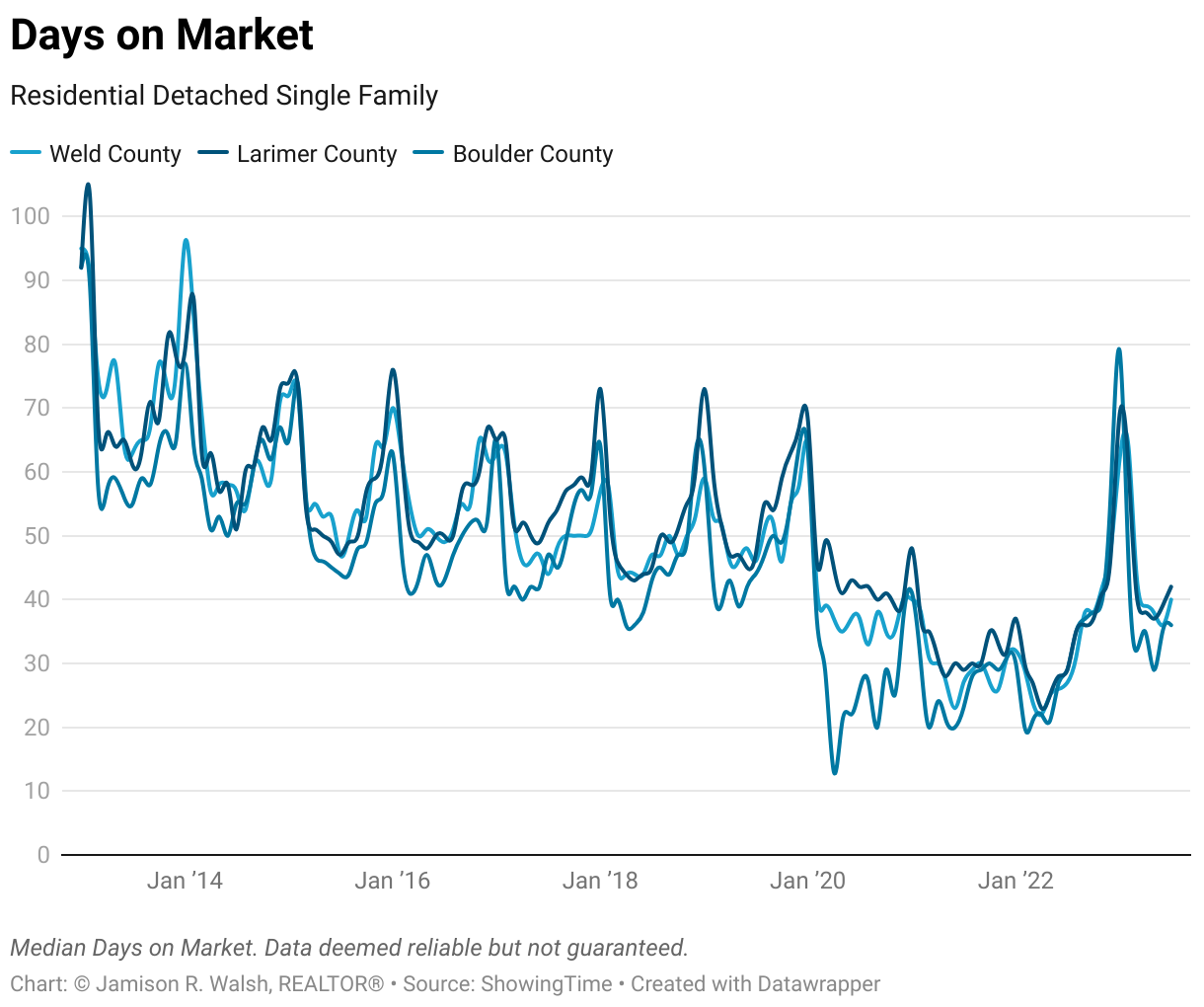

Regional Housing Metrics